All You Need to Know About API Banking

Author: Sankalp Tandon, Senior Solutions Consultant - Applied AI, Searce

The Indian banking sector is undergoing a massive digital shift. Why? First up is the widespread use of digital payments, bolstered by government initiatives for financial inclusion and a supportive regulatory framework.

This makes API banking a critical aspect for companies in the BFSI sector. This blog explores the concept of API banking, key trends driving the need for APIs in India, and why it is highly beneficial for banks & financial institutions.

So what is API banking?

API banking, also called open banking, is when banks and other financial companies let outside developers access their information and services. They do this through secure connections called APIs, which act like bridges between different systems. Basically, it allows other companies to build cool new apps and services using your bank's data (with your permission, of course!). This allows banks to extend their reach to the customers through third party developers who develop products with the bank's services integrated.

- Think of APIs like a shared language that lets bank computers and other companies' computers talk to each other. These APIs use special codes (like JSON or XML) to make sure information flows smoothly and securely between the two.

- API banking capability allows the partner to easily carry out banking transactions without switching between the enterprise resource planning (ERP) platform and the bank.

- Through this, banks have access to a broader customer base, thereby improving their reach. Additionally, it also helps banks to improve the relationship with customers through cross-sell / up-sell opportunities.

Since APIs are so useful for banks, they come in different types, each designed for specific tasks. Let's take a look at some of them:

- Open APIs are publicly available interfaces. They allow any developer to access and integrate banking functionalities into their applications. These APIs must adhere to strict regulatory requirements to ensure data security and customer protection. These APIs form the cornerstone of open banking.

- Internal APIs are used within financial institutions to improve efficiency and communication between different departments or systems. They help banks streamline operations and maintain control over sensitive data.

- Partner APIs are shared with specific business partners to enable collaborative services or products, offering a balance between openness and control. These APIs facilitate B2B communication and the development of value-added services.

Our focus for this blog will be the broader integrations of banking functionalities through open APIs and the real business outcomes that lie ahead.

Why should banks go for API banking?

Apart from enabling key integrations and functionalities, open banking presents important business cases for the banks. ICICI Bank and HDFC Bank, two of India's leading private-sector banks, have been pioneers in implementing API banking to enhance their digital offerings and streamline operations. Some of the benefits include:

- Improving customer reach and revenue streams: With API banking, banks can broaden their market reach. Consider ICICI Bank for example, they launched India's largest API banking portal, offering 250+ APIs across categories like payments, collections, etc. This move has accelerated partnerships with fintechs and e-commerce platforms, allowing ICICI Bank to attract a broader customer base by embedding banking services in non-banking ecosystems.

- Ease of partner onboarding: Time to onboard new partners is reduced through the use of standardized APIs & access to information via a centralized portal. For ICICI bank, the time to onboard new partners reduced from months to just a few days.

- Reduced customer acquisition cost: Banks/financial services providers get access to the customer base of the partners, reducing the customer acquisition cost. An Oliver Wyman article states the acquisition cost reduces from $100-200 to $5-$35 through access to broader customer base.

- Enhancing customer experience: API banking offers a seamless, embedded financial experience, improving customer satisfaction & retention. Through API integration, banks like ICICI & HDFC enable fintechs to deliver services such as instant payments, loans, & account management directly within their apps. This "anywhere banking" approach aligns with expectations of digital-first customers & increases engagement on both banking & non-banking platforms.

Not just the benefits. Several trends in the Indian banking landscape also point to the growing demand for API Banking

-

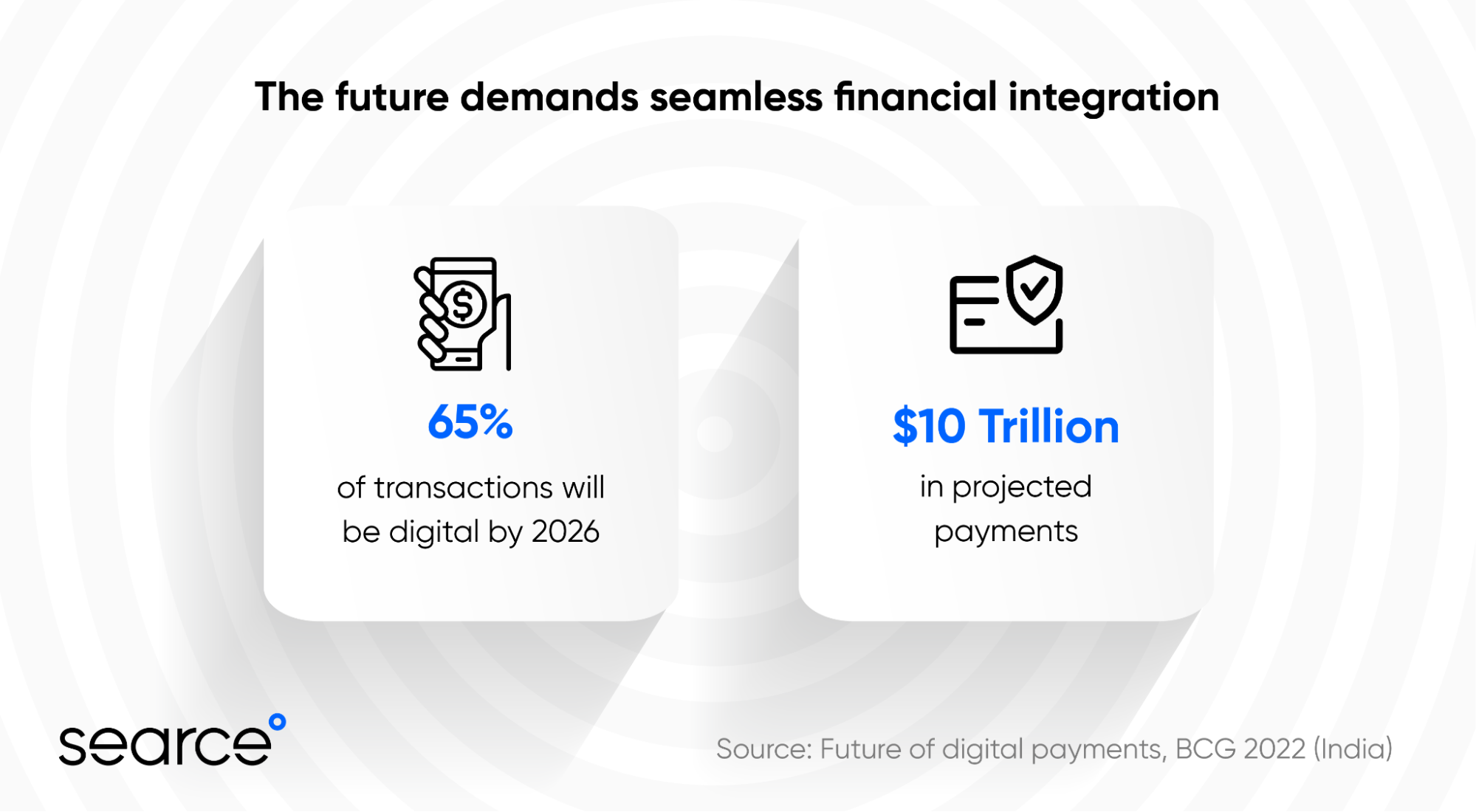

Massive growth in digital payments: India's digital payment sector is

booming, with UPI and digital merchant payment transactions leading the way. Digital

payments will constitute nearly 65% of all payments by 2026 and the projected transaction

value of $10 trillion by 2026 signifies a strong demand for seamless financial services

integrated into consumer platforms, a need that API banking can effectively address.

- Rising financial inclusion initiatives: India has made strides in bringing financial services to more people, but many are still left out, especially in rural areas. API banking can really help here. It allows companies that aren't banks to offer things like payments and loans digitally. This means people who haven't had access to traditional banking can now get the financial help they need, right from their phones. Government programs like Pradhan Mantri Jan Dhan Yojna, along with partnerships between different organizations, can make this even more effective.

- Supportive regulatory environment: Platforms like the Account Aggregator (AA) make it easy and safe for customers to share their financial information with other companies, like fintech apps. This creates a smooth flow of data between banks, these tech companies, and other financial institutions. Regulations like the Digital Personal Data Protection Act ensure improved customer data security while RBI's exploration of a Central Bank Digital Currency (CBDC) and expansion of UPI capabilities could further boost embedded finance adoption.

- Growth of fintech partnerships and embedded finance: The rise of fintech startups in India has led to innovative financial solutions often delivered through partnerships with traditional banks using API banking.

Challenges and imperatives for successful implementation of API banking

Financial institutions need to tackle important challenges to ensure successful implementation:

- Data Security and Privacy: When banks share data through open banking APIs, security is absolutely crucial. These APIs deal with very sensitive information like account details, transaction history, and even personal IDs. Sharing this kind of data with other companies increases the risk of fraud and breaches. That's why it's so important to have strong security in place, like encryption, multi-factor authentication (like a code sent to your phone), strict rules about who can access what, and constant monitoring for anything suspicious. These measures help keep customer data safe and prevent breaches. Also, it is essential to uphold customers' rights by transparently managing their data—letting them know how it is collected, stored, and utilized—and gettingtheir consent before any data sharing occurs.

- Focusing on end-to-end use cases and customer-centric design: Understanding customer needs is crucial before implementing any API Solutions. It is critical to ensure that these solutions address end-to-end use cases. This customer-centric approach ensures that APIs deliver value at every stage, enhancing customer experiences and promoting wider adoption.

- Compliance: Compliance is non-negotiable. It is not a one-time task but an ongoing process that requires continuous monitoring and adaptation. In India, Account Aggregator Framework, Digital Personal Data Protection Act, and Master Direction on Digital Payment Security Controls, etc. are some of the regulatory frameworks that aim to strengthen data security, safeguard sensitive financial data exchange and information, and provide a solid platform for open banking to thrive. However, to ensure constant adherence to these standards, financial institutions need to set up compliance programs to ensure adaptability of their systems and processes to the regulations.

- Upgrading from legacy systems: Legacy IT infrastructures can hinder the smooth implementation of API banking. Embracing modernization by adopting a cloud-native, API-led approach can help achieve the agility and scalability needed in the dynamic world of open banking. This transition enablesa more flexible and responsive architecture that can adapt to evolving customer demands and regulatory changes.

- Scalability and performance: APIs must be capable of handling high transaction loads without succumbing to latency issues or service disruptions, which can significantly impact customer satisfaction and trust. Employing techniques like API call optimization and intelligent caching can help minimize redundant data transfers, thereby improving response times and overall system efficiency.

- Technical integration and interoperability: One of the significant challenges in implementing open banking APIs is achieving seamless technical integration and interoperability across diverse platforms, systems, and providers. Open banking APIs facilitate data and service exchanges among various stakeholders, including banks, fintech companies, aggregators, merchants, and customers. This necessitates a high degree of compatibility, standardization, and alignment of infrastructure and protocols. Hence, APIs need to adhere to established best practices and frameworks, have a robust API design supported by rigorous testing and validation processes to identify and resolve potential issues proactively.

How can partners support clients implementing API banking

Partners like Searce can enable banks and financial services organisations to build, analyze, operate, and scale APIs in secure environments. Searce offers end-to-end solutions for API development and API management, with cost effective solutions deployed on cloud (Google Cloud/AWS) as well as on-premises.

-

Creating APIs for the banking products and services: We can develop APIs for banks to seamlessly deliver their products and services while managing the entire API lifecycle, including design, deployment, security, and monitoring. We ensure robust API security through OAuth, IP whitelisting, and granular access controls, etc., safeguarding sensitive financial data while complying with regulations. In addition, Searce guides banks in setting up robust API governance frameworks and implementing security best practices.

-

Creating and managing a front end API developer portal: We can develop an API portal to provide a way for the partners to access the bank's APIs based on their needs. In addition, we can also manage the API portal through monitoring and support, API versioning and updates, security & compliance management etc.

Don't take our word for it. Take a look at the real-world success stories of meaningful impact for companies like Ayoconnect and Zilch, where Searce enabled API-led transformation:

- Ayoconnect: Ayoconnect builds an open finance platform for developers to select from a range of financial products and deliver them to their customers. Faced with the need to provide a readily available set of open banking APIs, Ayoconnect partnered with Searce to implement their API management platform. This not only enabled the external exposure of their APIs, targeted to internal cloud services, but also provided a seamless developer experience through a custom-built portal with automated CI/CD pipelines. This significantly reduced development time and errors. The result was a robust API platform that allowed Ayoconnect to offer innovative services, achieve 99.8% uptime, automatic scalability during high traffic events & reduce development time.

- Zilch: Zilch is a payment service which aims to reduce the cost of consumer credit by providing varied payment options. Zilch needed to modernize their application architecture by splitting a monolith architecture into microservices via API and providing these APIs to third party partners through an API portal. Searce implemented a developer portal to expose proxies as products, along with API documentation and API key generation.

Building good APIs is more than just making them work; it's about creating a solid foundation that can grow and adapt as technology changes. Searce helps banks build this kind of strong API architecture, ensuring data is both easily accessible and highly secure. We help banks:

- Define exactly how their APIs can be used.

- Prioritize data protection.

- Make sure different systems can work together smoothly.

This lets them innovate and create better experiences for their customers.

Partnering with Searce gives you the tools and know-how to create secure, scalable, and even profitable API systems. This helps you transform your digital services, improve customer satisfaction, and succeed in the fast-changing world of API banking and embedded finance.

API banking is a fundamental change in how financial services are offered. As things move forward, API banking will become even more important, driving innovation, competition, and a focus on what customers want.